You can browse all the published concept maps without signing in. If you'd like to create your own concept maps, all you have to do is sign in with Twitter. It's free!

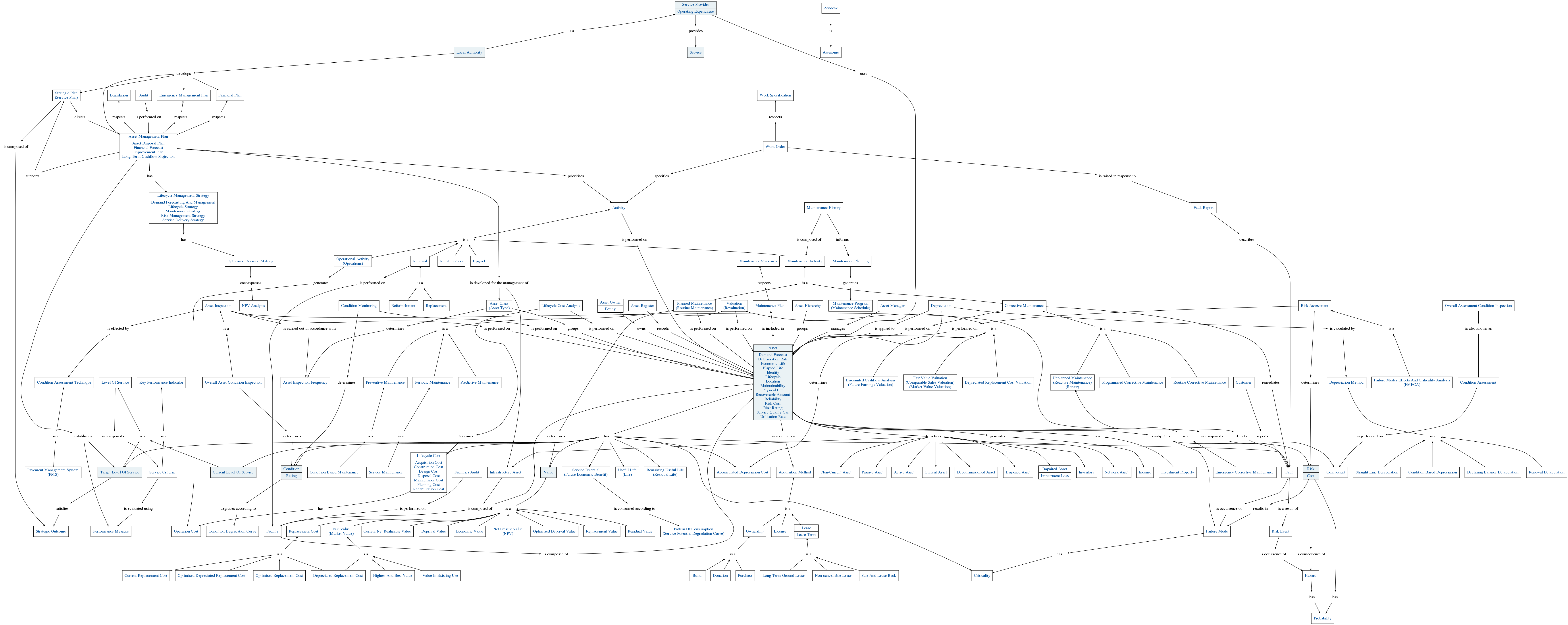

The goal of infrastructure asset management is to meet a required level of service, in the most effective manner, through the management of assets for present and future customers. IIMM

Accumulated depreciation is the total amount of depreciation charged to an asset from when it was first recognised to a given point in time. LGAM

Cost incurred as part of acquisition of an asset

Method by which an asset is acquired. Examples include purchase, lease, build.

Generally applies to above-ground assets (e.g. reservoir, pump station). DERM

An activity is the work undertaken on an asset or group of assets to achieve a desired outcome. IIMM

A physical component of a facility which has value,enables services to be provided and has an economic life of greater than 12 months. Dynamic assets have some moving parts, while passive assets have none. IIMM

An asset is an object (physical or intangible) that has an identifiable value and a useful life greater than 12 months, that is or could be used by the entity responsible for it to provide a service. LGAM

Asset - An item with an independent physical and functional identity and age, within a facility (e.g. pump, motor, sedimentation tank, main). Asset - Service potential or future economic benefits controlled by entity as a result of past transactions or other past events. DERM

An asset class is a grouping of assets of a similar nature and use. LGAM

An Asset Disposal Plan is a plan that documents the timing of, and the costs associated with the disposal of assets. It typically forms part of an Asset Management Plan. LGAM

A framework for segmenting an asset base into appropriate classifications. The asset hierarchy can be based on asset function; asset type or a combination of the two. IIMM

An asset hierarchy is a framework for segmenting an asset base into appropriate classifications. The asset hierarchy can be based on asset function; asset type or a combination of the two. LGAM

An Asset Condition Inspection is an inspection carried out on an asset to determine its condition.

Types of inspections:

There are two main types of asset condition inspections.

- Defect / hazard inspections designed to determine the need for maintenance and/or temporary works.

- More detailed overall asset condition inspections designed to assess the overall condition of an asset and determine its remaining useful life.

Defect / hazard inspections are typically carried out on a more frequent basis than overall asset condition inspections, but in both cases the inspection frequency may depend on the classification of the asset within a hierarchy. LGAM

The frequency with which planned asset inspections are performed.

A plan developed for the management of one or more infrastructure assets that combines multi-disciplinary management techniques (including technical and financial) over the lifecycle of the asset in the most costeffective manner to provide a specified level of service. A significant component of the plan is a long-term cashflow projection for the activities. IIMM

An Asset Management Plan (AMP) is a plan developed for the management of one or more infrastructure asset classes with a view to operating, maintaining and renewing the assets within the class in the most cost effective manner possible, whilst providing a specific level of service." LGAM

The entity which is responsible for managing the asset. May not be the same entity as the owner or the operator of the asset.

The owner of an asset is the person or entity that has exclusive rights and control over that asset, whether it be an object, land/real estate or intellectual property. LGAM

A record of asset information considered worthy of separate identification including inventory, historical, financial, condition, construction, technical and financial information about each. IIMM

An asset register is a database containing specific information about the assets owned or controlled by an organisation. LGAM

The focus of the audit is to check the Asset Management Plan has:

- well-defined justifiable levels of service

- minimum assumptions relating to asset information

- a robust AM improvement programme with task priorities and resource requirements identified

- an enhanced description of AM techniques used to establish the most cost-effective (optimum) asset lifecycle treatment options (i.e. risk management, > predictive modelling and optimised decision- making)

- quality presentation, including a stand-alone executive summary and extensive use of figures and tables

- a focused plan with extensive use made of appendices.

IIMM

Specific parts of an asset having independent physical or functional identity and having specific attributes such as different life expectancy, maintenance regimes, risk or criticality. IIMM

An item with an independent physical and functional identity within an asset (e.g. impeller, hydrant). DERM

Asset condition is a measure of the health of an asset. LGAM

The technique or process used to determine the condition of an asset. Varies depending on the type of asset.

A visual condition inspection is a common method of assessing an asset's condition by examining the external appearance of the asset. LGAM

LGAM lists the following examples:

Unlike traditional depreciation, which is based on a predetermined formula (approximating the rate of value decline), condition-based depreciation is a direct measure of the run down in asset value. Asset condition is measured by its deviation from 'as new'.

It is important to note that in many countries, the generally accepted accounting practices (GAAP) preclude the use of condition based depreciation in financial statements for external reporting purposes. IIMM

Condition-Based Depreciation is the determination of accumulated depreciation as the cost in any reporting period of restoring an asset's gross service potential, based on the condition of the asset within the period. Changes from year to year in cumulative depreciation so determined represent the annual depreciation. LGAM

The determination of accumulated depreciation as the cost in any reporting period of restoring an asset’s gross service potential, based on the condition of the asset within the period. Changes from year to year in the cumulative depreciation so determined represent the annual depreciation. DERM

Preventive maintenance initiated as a result of knowledge of an items condition from routine or continuous monitoring. IIMM

Condition based maintenance is a maintenance technique that involves monitoring the condition of an asset and using that information to predict its failure. Proactive Maintenance - Proactive maintenance is scheduled maintenance programmed on the basis of condition data. LGAM

The preventive maintenance initiated as a result of knowledge of the condition of an item from routine or continuous monitoring. (May also form part of predictive maintenance.) DERM

Describes the rate at which an asset's condition degrades over time.

Continuous or periodic inspection, assessment, measurement and interpretation of the resultant data, to indicate the condition of a specific component so as to determine the need for some preventive or remedial action. IIMM

Condition Monitoring is the continuous or periodic inspection, assessment, measurement and interpretation of the resultant data, to indicate the condition of a specific component so as to determine the need for some preventive or remedial action. LGAM

The continuous or periodic measurement and interpretation of data to indicate the condition of an item to determine the need for maintenance. DERM

Cost incurred as part of construction of an asset.

The remedial actions performed as a result of failure, to restore an item to a specified condition. Corrective maintenance mayor may not be programmed. IIMM

Corrective maintenance is maintenance carried out after a failure has occurred, and intended to restore an item to a state in which it can perform its required function. (This may include breakdown maintenance or reactive maintenance) LGAM

The maintenance carried out after a failure has occurred, and intended to restore an item to a state in which it can perform its required function. (This may include breakdown or reactive maintenance.) DERM

Cost is the amount of cash or cash equivalents paid or the fair value of the other consideration given to acquire an asset at the time of its acquisition or construction or, where applicable, the amount attributed to that asset when initially recognised in accordance with the specific requirements of other Australian Accounting Standards. LGAM

Cost (current) - An asset’s cost measured by reference to the lowest cost at which the gross service potential of the asset could currently be obtained in the normal course of events. (Synonymous with ‘gross current cost’.) Cost (replacement) - The cost of restoring an existing asset’s gross service potential on deprival, whether by reproduction of the existing asset or replacement with a reference asset. Cost (reproduction) - The cost of restoring an existing asset’s gross service potential on deprival by reproducing the existing asset. Cost (written down current) - An asset’s current cost less, where applicable, accumulated depreciation calculated on the basis of such cost to reflect the already consumed or expired service potential of the asset DERM

CRITICAL ASSETS Assets for which the the financial, business or service level consequences of failure are sufficiently severe to justify proactive inspection and rehabilitation. Critical assets have a lower threshold for action than noncritical assets. IIMM

Critical Assets - Critical assets are assets for which the financial, business or service level consequences of failure are sufficiently severe to justify proactive inspection and rehabilitation. Critical assets have a lower threshold for action than non-critical assets.

Criticality - Criticality is the quality, state, or degree of being of the highest importance. LGAM

Those assets which are expected to be realised in cash or sold or consumed within one year of an organisation's balance date. IIMM

A "current asset" is an asset which is expected to be consumed within one financial year. LGAM

The defined service quality for a particular activity (i.e. roading) or service area (i.e. streetlighting) against which service performance may be measured. Service levels usually relate to quality, quantity, reliability, responsiveness, environmental acceptability and cost. IIMM

The net value obtained upon sale. IIMM

The cost of replacing the service potential of an existing asset, by reference to some measure of capacity, with an appropriate modern equivalent asset.

IIMM

The cost of restoring an existing asset’s gross service potential on deprival, whether by reproduction of the existing asset or replacement with a reference asset.

DERM

Using the declining balance approach, the amount of depreciation reduces each year. The most common approach to this is to base the depreciation as a % of the book value or carrying value which decreases each year.

IIMM

DECOMMISSION Activities required to take an asset out of service.

IIMM

A projection of future demand for the use of an asset. Demand forecasts are usually wrong to a greater or lesser extent.

The active intervention in the market to influence demand for services and assets with forecast consequences, usually to avoid or defer CAPEX expenditure. Demand management is based on the notion that as needs are satisfied expectations rise automatically and almost every action taken to satisfy demand will stimulate further demand.

IIMM

The replacement cost of an existing asset less an allowance for wear or consumption having regard for the remaining economic life of the existing asset.

IIMM

The optimised replacement cost after deducting an allowance for wear or consumption to reflect the remaining or economic service life of the asset.

The wearing out, consumption or other loss of value of an asset whether arising from use, passing of time or obsolescence through technological and market changes. It is accounted for by the allocation of the cost (or revalued amount) of the asset less its residual value over its useful life. IIMM

Depreciation is the reduction in the value of an asset due to usage, passage of time, environmental factors, wear and tear, obsolescence, depletion or inadequacy. LGAM

The consumption of infrastructure and other assets is reported in financial statements as depreciation. Depreciation is the systematic allocation of the depreciable amount of an asset over its useful life. The depreciation method used is to reflect the pattern in which the asset's future economic benefits are to be consumed by the entity. There are at least 4 measures of asset consumption, each of which can be related to a method of depreciation:

- when consumption is constant over the useful life of the asset - straight line method,

- when consumption is greater in the early years and less in the later years - declining balance method,

- when consumption increases as the asset approaches the end of its useful life - output/service basis method,

- when consumption varies with outputs/service - units of production method.

AIFMG 2009

The method by which the degree of depreciation of an asset is calculated.

The value of an asset to the present owner if the owner were deprived of the asset and was required to continue to deliver the same level of service. Assets are valued at an amount that represents the entire loss that might be expected to be incurred if the entity were deprived of the service potential or future economic benefits of particular assets at the reporting date. This is a valuation basis that reflects a non-market concept of the value in use of assets as part of a going concern. IIMM

The "Deprival Value" of an asset is the value of the present owner if the owner were deprived of the asset and was required to continue to deliver the same level of service. Assets are valued at an amount that represents the entire loss that might be expected to be incurred if the entity were deprived of the service potential or future economic benefits of particular assets at the reporting date. This is a valuation basis that reflects a non-market concept of the value in use of assets as part of a going concern. LGAM

The value of an asset to the present owner. if the owner were deprived of the asset. Assets are valued at an amount that represents the entire loss that might be expected to be incurred if the entity were deprived of the service potential or future economic benefits of particular assets at the reporting date. If an entity no longer requires, or no longer intends, to provide a service, the nature of the asset changes and the measurement of the asset's deprival value may change. But the concept of deprival value remains applicable to the asset. This is a valuation basis that includes the non-market concept of the value in use of assets as part of a going concern. AIFMG 2009

DISCOUNTING A technique for converting cash flows that occur over time to equivalent amounts at a common point in time. DISCOUNT RATE A rate used to relate present and future money values, e.g. to convert the value of all future dollars to the value of dollars at a common point in time, usually the present.

IIMM

DISPOSAL Activities necessary to dispose of decommissioned assets.

IIMM

The period from the acquisition of the asset to the time when the asset, while physically able to provide a service, ceases to be the lowest cost alternative to satisfy a particular level of service. The economic life is at the maximum when equal to the physical life, however obsolescence will often ensure that the economic life is less than the physical life. IIMM

The Economic Life of an asset is the length of time for which maintaining and operating the asset remains the lowest cost alternative for providing a nominated level of service. LGAM

The period over which an asset is expected to be economically useable by one or more users or the number of production or similar units expected to be obtained from the asset by one or more users. AIFMG 2009

An assets discounted cashflow value derived by discounting the free cashflow of the asset by an appropriate risk adjusted discount rate. IIMM

The economic value of an asset is the discounted cashflow value derived by discounting the free cashflow of the asset by an appropriate risk adjusted rate. LGAM

The value of an asset deriving from its ability to generate income which is measured by discounting the net cashflow of the asset by an appropriate risk adjusted discount rate. For non-cash generating assets, the economic value is the value of the goods and services produced or provided to meet the entity's objectives. AIFMG 2009

The maintenance that is necessary to put in hand immediately to avoid serious consequences. (May also be called breakdown or reactive maintenance.)

DERM

The principal function of the Emergency Management Plan is to ensure the safety of the community by addressing the prevention of, response to and recovery from emergencies within a municipality.

The residual interest in the assets of the entity after deduction of its liabilities.

IIMM

see Failure Modes Effects And Criticality Analysis

The physical audit of a facility, usually required for valuation, lifecycle cost analysis, short-term maintenance planning and long-term planning purposes.

IIMM

A complex comprising many assets (e.g. a hospital, water treatment plant, recreation complex, etc.) which represents a single management unit for financial, operational, maintenance or other purposes.

IIMM

A facility is a group of assets located within a designated area that are associated in some way.

LGAM

Facility - A group of assets that provides a function or service (e.g. pump station, reservoir, treatment plant, reticulation system). Facility - A complex of assets (e.g. a hospital, water treatment plant, sporting complex) that represents a single management unit for financial, operational, maintenance or other purposes.

DERM

An asset's failure mode describes the way in which a failure occurs.

LGAM

A technique for analysing and evaluating a maintenance strategy or life-cycle strategy to ensure that the application has the desired reliability characteristics by obviating those critical failure modes through employment of redundancy, providing alternate modes of operation, de-rating, or any other means. - AIFMG 2009

The amount for which an asset could be exchanged, or a liability settled, between knowledgeable, willing parties in an arm's length transaction.

IIMM

Fair Value is "the amount for which an asset could be exchanged, or a liability settled, between knowledgeable, willing parties, in an arms length transaction." This is equivalent to the market value of the asset where one exists. If there is no market the fair value can be determined on a cost of acquisition basis.

LGAM

Fair Value is the best estimate of the price reasonably obtainable in the market at the date of valuation where a market exists. This is often not the case for existing infrastructure assets, in which case fair value is depreciated replacement cost.

AIFMG 2009

Valuation method which uses the prices achieved in sales of comparable assets to determine the value of the asset.

A defect of an asset which adversely affects its ability to safely provide a service.

A report which describes a fault relating to an asset.

Long-term financial plans take the funding projections for delivery of services from infrastructure, developed in asset management plans into a corporate financial plan covering all activities and services of the organisation. Long-term financial plans typically cover a period of 10 years. Accuracy and reliability of financial projections vary over the planning period ranging from good accuracy in the early years (1-3 years) to a lesser accuracy in the later years of the period. These relative accuracies are taken into account in annual updating and review of long-term financial plans. Based on the results of Australian local government financial sustainability reports, initial versions of the long-term financial plan may indicate that existing income levels will be insufficient in future to sustain existing service levels from infrastructure.

AIFMG 2009

The future economic benefit embodied in an asset is the potential to contribute, directly or indirectly, to the flow of cash and cash equivalents to the entity. OR In respect of not-for-profit entities, whether in the public or private sector, the future economic benefits are also used to provide goods and services in accordance with the entities' objectives.

LGAM

The future economic benefit embodied in an asset is the potential to conhibute directly, or indirectly, to the flow of cash or cash equivalents to the entity. The potential may be a productive one that is part of the operating activities of the entity. It may also take the form of convertibility into cash or cash equivalents or a capability to reduce cash outflows. For not-for-profit entities, whether in the public or private sector, the future economic benefits are also used to provide goods and services in accordance with the entity's objectives. Future economic benefits me synonymous with the notion of service potential and are used as a refcrence also to service potential. Future economic benefits can be described as the scarce capacity to provide benefits to the entities that use them and is common to all assets irrespective of their physical or other form.

AIFMG 2009

A hazard is any matter, thing, process or practice that may cause death, injury, illness or disease. LGAM

Where the valuer looks at alternative better uses for an asset and values it accordingly (this is required under International Financial Reporting Standards).

Identity refers to the ability to uniquely identify an individual asset.

"An asset is said to be impaired when its carrying amount exceeds its recoverable amount. Entities are required to make an assessment at the reporting date each year, if there are any indicators that an asset may be impaired. If so, the entity is to estimate the recoverable amount and recognise any impairment loss." - AIFMG 2009

The amount by which the carrying amount of an asset exceeds its recoverable amount. - AIFMG 2009

An Asset Management Improvement Plan is a strategic plan that provides for monitoring and control of the Asset Management Improvement Activites. It provides the link between the Asset Management Strategy and the annual operations plans and budgets. This plan will ensure that acceptable progress is made on improving asset management processes and procedures and that progress can be verified and quantified.

LGAM

Increases in economic benefits during the accounting period in the form of inflows or enhancements of assets or decreases of liabilities that result in increases in equity. other than those relating to contributions from equity participants (contributed capital). The definition of income encompasses both revenue and gains. Revenue arises in the course of the ordinary activities of an entity and is referred to by a variety of different names including sales, fees, interest, dividends, royalties and rent. Gains represent other items that meet the definition of income and may, or may not, arise in the course of the ordinary activities of the entity. Gains represent increases in economic benefit and include, for example, those arising on the disposal of non-current assets. • Capital income includes gain on disposal of non-financial assets, grants and contributions received specifically for new or upgraded assets and physical resources received free of charge, e.g. from a developer. • Operating Income is income shown in the Statement of Comprehensive Income other than capital income.

AIFMG 2009

Stationary systems forming a network and serving whole communities, where the system as a whole is intended to be maintained indefinitely at a particular level of service potential by the continuing replacement and refurbishment of its components. The network may include normally recognised ordinary assets as components.

IIMM

Infrastructure is any long-life physical asset that consists of an entire system or network (including components), not otherwise defined, which provides the foundation to support public services and enhance the capacity of the economy.

LGAM

Physical assets that contribute to meeting the needs of organisations or the need for access to major economic and social facilities and services, eg. roads, drainage, footpaths and cycleways. These are typically large. interconnected networks or portfolios of composite assets. The components of these assets may be separately maintained, renewed or replaced individually so that the required level and standard of service from the network of assets is continuously sustained. Generally the components and hence the assets have long lives. They are fixed in place and arc often have no separate market value.

AIFMG 2009

Assets held for sale in the ordinary course of business, in the process of production for such sale, or in the form of materials or supplies to be consumed in the production process or in the rendering of services.

AIFMG 2009

Property held to earn rentals or for capital appreciation or both, rather than for: (a) use in the production or supply of goods or services or for administrative purposes; or (b) sale in the ordinary course of business. AIFMG 2009

A qualitative or quantitative measure of a service or activity used to compare actual performance against a standard or other target. Performance indicators commonly relate to statutory limits, safety, responsiveness. cost, comfort, asset performance, reliability, efficiency, environmental protection and customer satisfaction.

AIFMG 2009

Acquisition of an asset by means of leasing it.

An agreement whereby the lessor conveys to the lessee in return for a series of payments the right to use an asset for an agreed period of time.

AIFMG 2009

The non-cancellable period for which the lessee has contracted to lease the asset, together with any further terms for which the lessee has the option to continue to lease the asset, with or without further payment, when at the inception of the lease it is reasonably certain that the lessee will exercise the option.

AIFMG 2009

The defined service quality for a particular activity (i.e. roading) or service area (i.e. streetlighting) against which service performance may be measured. Service levels usually relate to quality, quantity, reliability, responsiveness, environmental acceptability and cost.

IIMM

"Level of Service" can be defined as the service quality for a given activity. Levels of Service are often documented as a commitment to carryout a given action or actions within a specified time frame in response to an event or asset condition data.

LGAM

A measure of the anticipated life of an asset or component; such as time, number of cycles, distance intervals, etc.

AIFMG 2009

The cycle of activities that an asset (or facility) goes through while it retains an identity as a particular asset i.e. from planning and design to decommissioning or disposal.

IIMM

Life cycle has two meanings: 1. The cycle of activities that an asset (or aggregation of assets) goes through while it retains an identity as that asset. These activities include planning, design, acquisition and support, including rehabilitation and disposal. 2. The period of time between a selected date and the cut-off year or last year, over which the criteria (e.g. costs) relating to a decision or alternative under study will be assessed.

DERM

The total cost of an asset throughout its life including planning, design, construction, acquisition, operation, maintenance, rehabilitation and disposal costs.

IIMM

The term Lifecycle Cost refers to the total cost of ownership over the life of an asset including; planning, design, construction/acquisition, operation, maintenance, renewal, finance and disposal costs.

LGAM

The total cost of an asset throughout its life including planning, design, acquisition, operations, rehabilitation and disposal costs.

DERM

Any technique which allows assessment of a given solution, or choice from among alternative solutions, on the basis of all relevant economic consequences over the service life of the asset.

IIMM

Lifecycle Cost Analysis is a method of assessing which asset option, will be the most economical over an extended period of time.

LGAM

An organisation such as a Local Council that is responsible for the management of infrastructure assets in a defined local area.

Through the use of long-term ground leases organisations secure a future strategic asset while facilities are provided by private companies. Upon termination of the lease the lessor has the right for the building ownership to be transferred to the leaseholder or demolished and grounds reinstated. - IIMM

A characteristic of design and installation usually identified by the time and effort that will be required to retain an asset as near as practicable to its new or desired condition within a given period of time.

AIFMG 2009

All actions necessary for retaining an asset as near as practicable to its original condition, but excluding rehabilitation or renewal. Fixed interval maintenance is used to express the maximum interval between maintenance tasks. On-condition maintenance is where the maintenance action depends upon the item reaching some predetermined condition.

IIMM

Maintenance is any activity performed on an asset with a view to ensuring that it is able to deliver an expected level of service until it is scheduled to be renewed, replaced or disposed of.

LGAM

The combination of all technical and associated administrative actions intended to retain an item in, or restore it to, a state in which it can perform its required function.

DERM

Cost incurred as part of maintenance of an asset.

A history record which is used for the purpose of maintenance planning.

DERM

Collated information, policies and procedures for the optimum maintenance of an asset, or group of assets.

IIMM

Deciding in advance the jobs, methods, tools, machines, labour time required, and timing of maintenance actions.

DERM

A maintenance program is a time-based plan allocating specific maintenance tasks to specific periods

LGAM

Maintenance program - A time-based plan allocating specific maintenance tasks to specific periods.

DERM

Maintenance schedule - A comprehensive list of items and the maintenance required, including the intervals at which maintenance should be performed.

DERM

The standards set for the maintenance service, usually contained in preventive maintenance schedules, operation and maintenance manuals, codes of practice, estimating criteria, statutory regulations and mandatory requirements, in accordance with maintenance quality objectives.

IIMM

The estimated amount at which an asset would be exchanged on the date of valuation, between a willing buyer and a willing seller, in an arm's length transaction after proper marketing, and when the parties have each acted knowledgeably, prudently and without compulsion. Market value is based on highest and best use of the asset and not necessarily the existing uses.

IIMM

The value of an asset to the organisation, derived from the continued use and subsequent disposal in present monetary values. It is the net amount of discounted total cash inflows arising from the continued use and subsequent disposal of the asset after deducting the value of the discounted total cash outflows.

IIMM

A network asset is an asset that is considered to be part of a network. Network assets are interconnected assets that rely on each other to provide a service. If a network asset is removed the system may not function to full capacity.

LGAM

Individual asset which, together with others, performs a service.

DERM

All assets other than current assets, including assets held but not traded by a business in order to carry out its activities. Such assets are intended for use, not exchange, and normally include physical resources such as land, buildings, drains, parks, water supply and sewerage systems, furniture and fittings.

IIMM

An asset of a business which is expected to be consumed over more than one financial year.

DERM

A lease that is cancellable only upon the occurrence of some remote contingency, or with the permission of the lessor, or if the lessee enters into a new lease for the same or an equivalent asset with the same lessor, or upon payment by the lessee of such an additional amount that, at the inception of the lease, makes the continuation of the lease reasonably certain. AIFMG 2009

recurrent expenditure, which is continuously required to provide a service. In common use the term typically includes, eg power, fuel, staff, plant equipment, on-costs and overheads but excludes maintenance and depreciation. Maintenance and depreciation is on the other hand included in operating expenses. AIFMG 2009

Cost incurred as part of operation of an asset.

The active process of utilising an asset which will consume resources such as manpower, energy, chemicals and materials. Operation costs are part of the lifecycle costs of an asset.

IIMM

The active process of utilising an asset which will consume resources such as manpower, energy, chemicals and materials. Operation costs are part of the lifecycle costs of an asset. IIMM

Operation is the act of utilising an asset. Asset operation will typically consume materials and energy. LGAM

Regular activities to provide services such as public health, safety and amenity, eg street sweeping, grass mowing and street lighting. AIFMG 2009

(ODM) Two definitions are: 1. ODM is a formal process to identify and prioritise all potential solutiuons with consideration of financil viability, social and environmental responsibility and cultural outcomes. 2. An optimisation process for considering and prioritising all options to rectify existing or potential performance failure of assets. The process encompasses NPV analysis and risk assessment.

IIMM

(ODRC) The optimised replacement cost after deducting an allowance for wear or consumption to reflect the remaining economic or service life of an existing asset. ODRC is the surrogate for valuing assets in use where there are no competitive markets for assets, or for their services or outputs.

IIMM

(ODV) This is a set of rules, rather than a valuation approach, which describe the value boundaries for specified assets employed in monopoly markets. The rules are a combination of a cost based approach (ODRC) and the economic value where the ODV is taken to be the lowest of these.

IIMM

(ORC) The minimum cost of replacing an existing asset with modern equivalent assets offering the same level of service. The optimisation process adjusts the value for technical and functional obsolescence, surplus assets or over-design.

IIMM

Asset inspection performed to determine the overall condition of an asset, may also be performed for the purposes of valuation or depreciation calculation.

overall asset condition inspections (are) designed to assess the overall condition of an asset and determine its remaining useful life - LGAM

A degradation curve is a graph of an asset's condition or remaining service potential plotted over time.

LGAM

(PMS) A systematic process for measuring and predicting the condition of road pavements and wearing surfaces over time and recommending corrective actions.

AIFMG 2009

Periodic Maintenance is maintenance that is conducted on a predetermined schedule.

The life until the asset ceases to provide the required level of service because of physical deterioration of the asset.

Planned maintenance activities fall into three categories: i) Periodic - necessary to ensure the reliability or to sustain the design life of an asset. ii) Predictive - condition monitoring activities used to predict failure. iii) Preventive - maintenance that can be initiated without routine or continuous checking (e.g. using information contained in maintenance manuals or manufacturers' recommendations) and is not condition-based.

IIMM

Planned maintenance is maintenance organised and carried out with forethought, controland the use of records to a predetermined plan.

LGAM

The maintenance organised and carried out with forethought, control and the use of records to a predetermined plan.

DERM

Repair work that is identified and managed through a maintenance management system (MMS). MMS activities include inspection, assessing the condition against failure breakdown criteria/experience, prioritising scheduling, actioning the work and reporting what was done 10 develop a maintenance history and improve maintenance and service delivery performance.

AIFMG 2009

Predictive Maintenance is maintenance that aims to gather information about the likely degradation in asset performance in the future.

Preventive maintenance is maintenance carried out at predetermined intervals, or corresponding to prescribed criteria, and intended to reduce the probability of failure or the performance degradation of an item.

LGAM

The maintenance carried out at predetermined intervals, or corresponding to prescribed criteria, and intended to reduce the probability of failure or the performance degradation of an item.

DERM

The probability of some event occurring. Usually expressed as a percentage chance over some period of time.

Maintenance required within a short time period to return the asset to the standard in which it can properly and reliably function. In order to return the item to its original condition and significance.

A value representing the condition of an asset, usually corresponding to an assessment of the asset's remaining useful life.

5, 10 & 11 Category Condition Rating Systems are the most common, but other systems have been used, and each system has its pros & cons. - LGAM

"Reactive Maintenance" is a form of maintenance in which equipment and facilities are repaired only in response to a breakdown or a fault.

LGAM

The maintenance that is necessary to put in hand immediately to avoid serious consequences. (May also be called breakdown or emergency maintenance.)

DERM

Unplanned repair work that is carried out in response to service requests and management/supervisory directions.

AIFMG

Is the greater of the amount recoverable from an asset's further use and ultimate disposal, and its current net realisable value.

IIMM

Recoverable Amount is an accounting term referring to the price an asset would it would fetch if sold, or its value to the company when used, whichever is the larger figure.

LGAM

Work performed on an asset to sustain the delivery of a specified level of service.

Works to rebuild or replace parts or components of an asset, to restore it to a required functional condition and extend its life, which may incorporate some modification. Generally involves repairing the asset to deliver its original level of service (i.e. heavy patching of roads, sliplining of sewer mains, etc.) without resorting to significant upgrading or renewal, using available techniques and standards.

IIMM

Rehabilitation is "works carried out to rebuild or replace parts or components of an asset, to restore it to a required functional condition and extend its life, which may incorporate some modification.

LGAM

Works to rebuild, or replace parts of components of, an asset to restore it to the required functional condition and/or extend its life. This could also incorporate some modification. Generally involves repairing the asset to deliver similar function using available techniques and standards (i.e. not a significant upgrade or renewal). Examples include heavy patching of roads and slip-lining of sewer mains.

DERM

Cost incurred as part of rehabilitation of an asset.

The ability of an item to perform a required function under stated conditions for a stated period of time.

DERM

The Remaining Useful Life (RUL) of an asset is the estimated length of time remaining before it will need to be replaced.The Remaining Useful Life (RUL) of an asset is the estimated length of time remaining before it will need to be replaced.

LGAM

Works to upgrade, refurbish or replace existing facilities with facilities of equivalent capacity or performance capability.

IIMM

Renewal is the replacement or refurbishment of an existing asset (or component) with a new asset (or component) capable of delivering the same level of service as the existing asset.

LGAM

Works completed to upgrade facilities significantly from the existing asset.

DERM

Pure renewal accounting occurs when an asset is held at historical cost or at the latest valuation, and no depreciation is charged, but any renewal expenditure is treated as operational expenditure in the year of expense. As with condition-based depreciation, in many countries generally accepted accounting practices (GAAP) preclude the use of renewal accounting for financial reporting purposes.

IIMM

Action to restore an item to its previous condition after failure or damage.

IIMM

Action to restore an item after failure or damage.

DERM

The complete replacement of an asset that has reached the end of its life, so as to provide a similar, or agreed alternative, level of service.

IIMM

Replacement is the complete replacement of an asset that has reached the end of its life. so as to provide a similar or agreed alternative level of service.

LGAM

Complete removal and use of another item in place of an asset that has reached the end of its life, so as to provide a similar or agreed level of service.

DERM

The cost of replacing an existing asset with a substantially identical new asset.

IIMM

The "Replacement Cost" (also Replacement Value & Capital Replacement Value) of an asset is the cost of replacing it with a substantially identical new asset.

LGAM

The net market or recoverable value which would be realised from disposal of an asset or facility at the end of its life.

IIMM

The residual value (salvage value) of an asset is the estimated amount that an entity would currently obtain from disposal of the asset, after deducting the estimated costs of disposal, if the asset were already of the age and in the condition expected at the end of its useful life. - AASB 116.

LGAM

Residual value is the estimated amount that an entity would currently obtain from disposal of an asset, after deducting the estimated costs of disposal, if the asset were already at the end of its useful life. Residual value may be recognised in infrastl1lcture in certain circumstances such as where the asset has a salvage value and/or cost to renew an asset is less that the cost to replace the asset. Residual value may be used to relate the asset's asset management practices and procedures to its accounting treatment.

AIFMG 2009

Regular revaluation is often mandated for infrastructure intensive organisations and is also a requirement with the adoption of the 'revaluation model' option under AASB 116 Property, Plant and Equipment. The revaluation model requires an item of property, plant and equipment whose fair value can be measured reliably, to be carried at a revalued amount, being its fair value at the date of the revaluation less any subsequent accumulated depreciation and subsequent accumulated impairment losses. Revaluations are to be made with sufficient regularity to ensure that the carrying amount does not differ materially from that which would be determined using fair value at the reporting date. When an item of property, plant and equipment is revalued, the entire class of property, plant and equipment to which that asset belongs is to be revalued.

AIFMG 2009

A risk is the probability of a failure of an asset as a result of the occurrence of a hazard. There may be a resulting cost associated with the risk.

A risk assessment is a process that to used to assess the risks associated with a hazard.

LGAM

The assessed annual cost or benefit relating to the consequence of an event. Risk cost equals the costs relating to the event multiplied by the probability of the event occurring.

IIMM

A risk event is an occurrence of a hazard. For example, Hurricane Katrina was an occurrence of the hurricane hazard.

A risk rating is an indication of the relative risk associated with an asset. The rating may be determined using a number of factors such as: * the likelihood of failure * the severity of the consequences of a failure * the financial impact of a failure

Risk ratings may be numeric or labels such as:

Low, Moderate, Significant, High - IIMM

Corrective maintenance, excluding emergency corrective and programmed corrective maintenance.

IIMM

Day-to-day operational activities to keep the asset operating (replacement of light bulbs, cleaning of drains, repairing leaks, etc.) and which form part of the annual operating budget, including preventive maintenance.

IIMM

This model involves an organisation purchasing land and constructing the facility, selling on completion, then the organisation leasing the property back. This enables the facilities to be provided at no capital cost and the lease costs to be matched with the benefits delivered. - IIMM

A system supplying a public need such as transport, communications, or utilities such as electricity and water.

Service undertaken seasonally or annually to enable the required level of service to be delivered.

IIMM

For public sector (not-for-profit) organisations, service planning is the process of determining the services needed by a community (the organisations' customers). Service planning may include strategic planning for a community covering a period of 20 - 50 years, determining the services required to achieve the strategic community outcomes, engaging with the community to determine the optimum levels of service to suit available resources, determining how the services are to be provided and what measures are to be used to measure progress on achieving community outcomes. Service planning can assist organisations in many ways by answering the following questions:

- where are we now?

- where do we want to go?

- how do we get there?

- how do we know we are there?

Service plans are an essential tool in rational and co-ordinated decision making about levels and type of services where resources, funding, people and assets are used through clear links to long term financial planning. Good service plans:

- provide a route map to outcomes prioritised by the community,

- assist in identifying and managing risks in service delivery, and

- ensure that community and customer needs are met. Service planning is important as its outcomes affect the community' s quality of life.

AIFMG 2009

The total future service capacity of an asset. It is normally determined by reference to the operating capacity and economic life of an asset.

IIMM

Service potential is the total future service capacity of an asset. It is normally determined by reference to the operating capacity and economic life of an asset.

LGAM

A degradation curve is a graph of an asset’s condition or remaining service potential plotted over time. LGAM

An organisation responsible for providing a service.

In the straight line approach the depreciation charge remains fixed over the life of the asset, except where revaluations occur or useful lives are reassessed.

Where the pattern of economic consumption does not materially differ from straight line, or where the pattern cannot be reasonably determined and demonstrated, straight-line depreciation is considered a reasonable approximation.

IIMM

Straight-line depreciation is a depreciation method that results in a constant reduction of an assets written down value over the useful life of the asset, providing its residual value does not change.

LGAM

A plan containing the long-term goals and strategies of an organisation. Strategic plans have a strong external focus, cover major portions of the organisation and identify major targets, actions and resource allocations relating to the long-term survival, value and growth of the organisation. IIMM

The Financial Management Standard 1997 requires asset strategic planning to be undertaken by agencies as part of their strategic and operational planning processes. The asset strategic plan links with other strategic plans of the agency including finance, human resources and information systems as enabling strategies for the delivery of the agency's core services. A Strategic Asset Management Plan (SAMP) is a plan that documents service standards (set by the service provider) as well as an operations, maintenance and renewals strategy for achieving these standards. LGAM

The defined service quality for a particular activity (i.e. roading) or service area (i.e. streetlighting) against which service performance may be measured. Service levels usually relate to quality, quantity, reliability, responsiveness, environmental acceptability and cost.

IIMM

Corrective work required in the short-term to restore an asset to working condition so it can continue to deliver the required service or to maintain its level of security and integrity.

IIMM

Breakdown Maintenance is maintenance that is performed on an asset after it has failed. "Unplanned Maintenance" is maintenance carried out to no predetermined plan.

LGAM

An upgrade is capital works carried out on an existing asset to provide a higher level of service.

LGAM

May be expressed as either: (a) The period over which a depreciable asset is expected to be used, or (b) The number of production or similar units (i.e. intervals, cycles) that is expected to be obtained from the asset.

IIMM

The "useful life" (UL) of an asset is the estimated length of time during which the asset is able to deliver a given level of service.

LGAM

The rate at which the services provided by the asset are consumed.

Assessed asset value which may depend on the purpose for which the valuation is required, i.e. replacement value for determining maintenance levels, market value for lifecycle costing and optimised deprival value for tariff setting.

IIMM

A valuation is the determination of the economic value of an asset.

LGAM

The current value of a non-current asset of a local government is the loss that it would incur if it were deprived of the asset’s utility (or service potential). (Synonymous with ‘deprival value’.)

DERM

The value that specific assets contribute to the organisation of which they are a part, without regard to the assets' highest and best use, or the monetary amount that might be realised upon a sale. It is the value a specific asset has for a specific use to a specific user and is therefore non-market related.

IIMM

A written instruction detailing work to be carried out.

DERM

A document describing the way in which work is to be carried out. It may define the materials, tools, time and standards.

DERM

This concept map is owned by jimmyjazz68

Other users collaborating on this concept map:

{kind=link}