You can browse all the published concept maps without signing in. If you'd like to create your own concept maps, all you have to do is sign in with Twitter. It's free!

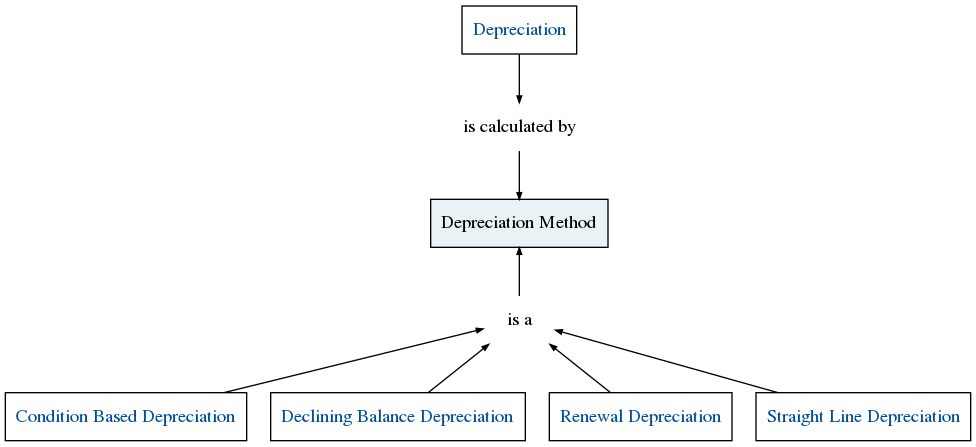

The method by which the degree of depreciation of an asset is calculated.

Unlike traditional depreciation, which is based on a predetermined formula (approximating the rate of value decline), condition-based depreciation is a direct measure of the run down in asset value. Asset condition is measured by its deviation from 'as new'.

It is important to note that in many countries, the generally accepted accounting practices (GAAP) preclude the use of condition based depreciation in financial statements for external reporting purposes. IIMM

Condition-Based Depreciation is the determination of accumulated depreciation as the cost in any reporting period of restoring an asset's gross service potential, based on the condition of the asset within the period. Changes from year to year in cumulative depreciation so determined represent the annual depreciation. LGAM

The determination of accumulated depreciation as the cost in any reporting period of restoring an asset’s gross service potential, based on the condition of the asset within the period. Changes from year to year in the cumulative depreciation so determined represent the annual depreciation. DERM

Using the declining balance approach, the amount of depreciation reduces each year. The most common approach to this is to base the depreciation as a % of the book value or carrying value which decreases each year.

IIMM

The wearing out, consumption or other loss of value of an asset whether arising from use, passing of time or obsolescence through technological and market changes. It is accounted for by the allocation of the cost (or revalued amount) of the asset less its residual value over its useful life. IIMM

Depreciation is the reduction in the value of an asset due to usage, passage of time, environmental factors, wear and tear, obsolescence, depletion or inadequacy. LGAM

The consumption of infrastructure and other assets is reported in financial statements as depreciation. Depreciation is the systematic allocation of the depreciable amount of an asset over its useful life. The depreciation method used is to reflect the pattern in which the asset's future economic benefits are to be consumed by the entity. There are at least 4 measures of asset consumption, each of which can be related to a method of depreciation:

- when consumption is constant over the useful life of the asset - straight line method,

- when consumption is greater in the early years and less in the later years - declining balance method,

- when consumption increases as the asset approaches the end of its useful life - output/service basis method,

- when consumption varies with outputs/service - units of production method.

AIFMG 2009

Pure renewal accounting occurs when an asset is held at historical cost or at the latest valuation, and no depreciation is charged, but any renewal expenditure is treated as operational expenditure in the year of expense. As with condition-based depreciation, in many countries generally accepted accounting practices (GAAP) preclude the use of renewal accounting for financial reporting purposes.

IIMM

In the straight line approach the depreciation charge remains fixed over the life of the asset, except where revaluations occur or useful lives are reassessed.

Where the pattern of economic consumption does not materially differ from straight line, or where the pattern cannot be reasonably determined and demonstrated, straight-line depreciation is considered a reasonable approximation.

IIMM

Straight-line depreciation is a depreciation method that results in a constant reduction of an assets written down value over the useful life of the asset, providing its residual value does not change.

LGAM

{kind=link}